The BCRA Gold Reserves "Mystery"

The details around Argentina's gold reserves and recent precedents

Welcome Avatar! Much ink was spilled on Milei’s decision to move part of Argentina’s gold offshore in order to get yield on those reserves. Why did international media outlets start crying without checking precedents or the BCRA balance sheet with the details? Let’s dig in.

Where Does the Yield Come From?

Most might already know this, but as an introduction it is useful to understand that Central banks can generate yield on gold reserves in the following ways:

There are two ways in which a central bank can generate yield from its gold holdings. The first is through the uncollateralised lending of gold, most commonly to a bullion bank. Given that gold is a monetary asset for central banks, it can be lent out on term deposit in the same way as any other currency in their reserve portfolio. Typically, a central bank will place gold on deposit with a bullion bank, in return for a deposit rate. Maturities vary but the most frequent are 1-month, 3-month and 12-month tenors. At the end of the term, the gold is returned with the interest paid either in gold or currency, although the bars will be different from those originally lent out. Deposit rates are derived and set independently by bullion banks.

Central banks are also able to generate yield from their gold holdings via a gold swap, or more specifically, a repurchase agreement that simulates a swap. In this transaction, a central bank sells its gold to a bullion bank with the promise to buy back the gold at a later date. The central bank pays interest equivalent to the GOFO rate so, in this context, the GOFO rate could be understood as a US dollar loan using gold as collateral. Officially, it is defined as the rate at which market-making members of the London Bullion Market Association (LBMA) will lend gold on swap against US dollars. The central bank is then able to reinvest the funds at Libor and earn the spread between Libor and GOFO, which in this case will amount to the gold lease rate. — Source

With that out of the way, let’s dive into the specifics of the BCRA case moving part of its gold reserves abroad.

The BCRA Move

Last month, some clickbait article headlines in CNN and El País went viral on social media stating that “The Argentine Central Bank confirms the shipment of gold abroad, but does not specify the amount, destination or reasons”.

If the publication time on the articles is correct, then CNN basically copied the El País headline word for word:

These headlines are disingenuous to say the least. Bloomberg was a bit less tendentious and titled with “Argentina Ships Gold Bars Abroad to Be Financially Certified”.

For starters, roughly 60% of Argentina's gold reserves have been sent abroad in recent years, and the majority before Milei’s presidency. The headlines make it seem as if Milei decided to send most of the BCRA reserves abroad.

In reality, the Minister of Economy only sent six tons abroad in this year, completing a total of 31 tons located offshore.

The Milei government explained that this year’s gold operation provides the entity with tools to generate returns by depositing the metal abroad or, if required, use it as collateral to obtain liquid dollars through the Bank for International Settlements (BIS).

As mentioned in the previous article Pesos no More in July:

President Milei knows that debt payments could become an issue next year, and assured that he already has a “repo ready for next year” to pay the maturities in case the rollover he is seeking fails: “If we don't manage to secure a rollover, that repo will cover it.”

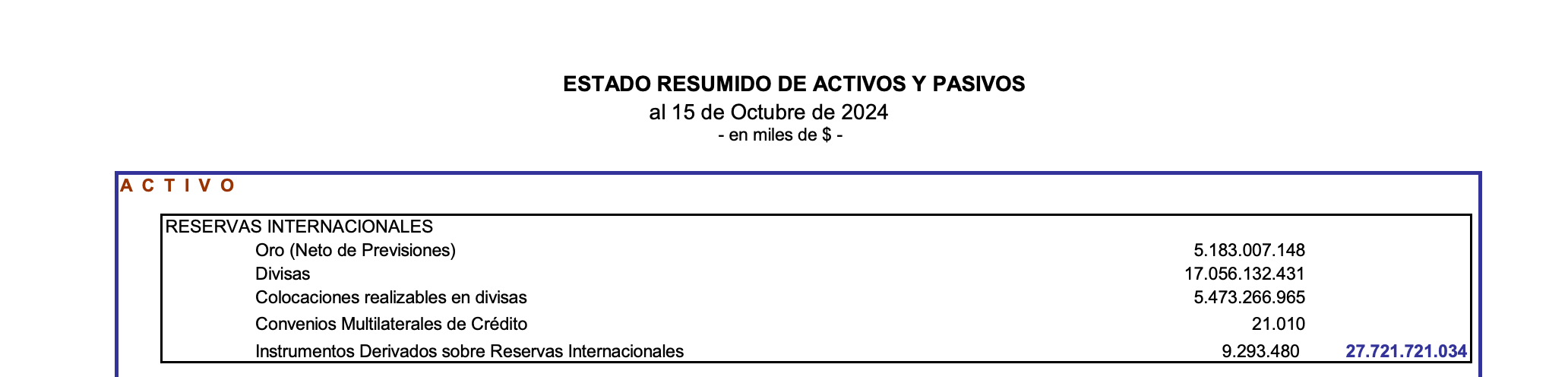

The BCRA has approximately 4.7 billion dollars in bullion gold (physical) that does not yield any interest.

In order for that money to yield something, the BCRA has now lent out 10% of its gold holdings (paper gold). This way, Argentina can charge interest and use that gold as collateral in potential debt negotiations.

Bloomberg published this almost 2 months later:

Argentina’s central bank sent part of its gold reserves abroad in recent weeks to be validated for financial use, a move that could give the country some much-needed flexibility, according to people with direct knowledge of the matter.

Once certified, the gold could eventually be used as collateral to obtain financing, according to one of the people, who asked not to be identified discussing private information. Before the move, about half of Argentina’s gold was in domestic vaults with the other half in London, another person said.

Precedents

This is not the first time that this type of investment has been made with BCRA gold. The first was in October 2016 under the management of Federico Sturzenegger at the BCRA under the Macri presidency — Minister of Deregulation in the Milei government — , who made a swap with 5 tons of gold, which was renewed in February 2017. The BCRA made several similar trades afterwards, that never exceeded 10% of the total gold reserves.

Even during the previous Alberto Fernández government in March 2020, a swap was made with 5 tons that returned in April, and in December 2021 a similar transaction was made with 7 tons that returned a month later.

The BCRA does not provide the details around these swap and repo transactions and does so only after the fact, which tends to cause media speculation on how much reserves are actually still held by the central bank.

In September 2023, the BCRA came out with a statement — which turned out to be correct —, after much media speculation around the state of the gold reserves under Alberto Fernández’s presidency:

“The BCRA balance sheet reflects regular financial operations to improve the profitability of reserves. These operations include all assets held by the BCRA and are audited internally and externally.

In the case of gold, the BCRA maintains the same position in this metal. This is not the first time that the idea has been attempted to be introduced that the BCRA has divested itself of its gold holdings.

This did not happen in the past, nor did it happen on this occasion. Payments to the IMF were made as reported, with bridge loans from CAF and yuan.”

A similar thing is happening now under Milei. It all depends on which outlets are writing about it, and from what angle.

Javier Lorca in El País wrote:

The uncertainty of what the far-right government is doing with gold reserves arose this July, when the bank workers' union, known as La Bancaria, warned about the transfer of bullion.

[…]

In the absence of official data, the La Bancaria union had filed a request for access to public information and opposition legislators had demanded that the officials involved explain what was being done with the gold.

Remember: whenever someone uses “ultra-right wing” or “far-right” like Lorca here, their credibility and motives should be seriously questioned.

The bankers union he mentions, well… we don’t really need to ask why that union never raised an eyebrow during the gold swaps and repos when Sergio Massa was Minister of Economy.

Bloomberg decided to put some more fuel on the gold fire:

Officials from the central bank, known by its Spanish acronym BCRA, declined to comment on the matter.

The monetary authority separately confirmed Monday it had sent gold between its accounts, mentioning both ones in the country and others abroad. However, the bank didn’t say how much of its nearly $5 billion in gold was shipped, for what reason or to where.

If these journalists would simply do their job, they would know that over the last few years, the BCRA has reportedly had some 37 tons of gold deposited in London, which would be part of various swap operations used to obtain financing. This recent move is simply adding more to those reserves located abroad.

This is not new, and it’s interesting they never mentioned anything of the sort during either the Macri or Alberto Fernandez presidencies.

An official BCRA communication last month underlined this hypocrisy as well:

The BCRA expresses its concern about the irresponsible dissemination of information for political purposes related to these operations before their completion, as it put the security of the assets of all Argentines at risk.

Information on the management of the BCRA's reserves has always been handled confidentially in an effort to preserve their security.

Both the General Audit Office of the Nation and the relevant control entities maintain access to this information under the same cloak of confidentiality.

The Central Bank stated that these “rebalancing operations do not alter the total volume of gold reserves, which remain equivalent to approximately US$4,981 million as published in the balance sheet of August 23, 2024.”

When comparing that number to the numbers published by the BCRA in October, the gold reserves remain stable, at $5.18 billion USD after the latest gold price increase:

Liquidity & Maturities

In Argentina’s case, it makes perfect sense to do this. There are no new international dollar loans on the horizon, and the maturities in 2025 are not going to pay themselves.

“The movement of gold is a matter of efficient reserve management. You can keep the gold physically or in deposit. If these reserves are physically held, they are immobilized. If they are at the BIS, you can earn some interest on the deposit, leverage it, make it liquid via collateral or sell it.” — Source

Gold located outside the country is the easiest to use for a swap and transform into money. The gold located in Buenos Aires, meanwhile, can take a couple of days before it could be used.

When looking at the maturities coming up, January and July 2025 will be the most complicated months where a swap might come in handy:

Unfortunately someone has to pay for the helicopter money party that has gone on for so many years, and it usually isn’t the ones throwing it out of the chopper.

Potential Downsides

There is always a risk that gold held abroad could be embargoed, as happened in 2019 with the 30 tons of gold Venezuela held at the Bank of England (BoE).

Venezuela’s gold is not officially seized, but frozen, since the BoE claims that the ownership of the gold is not verified after Maduro’s fraudulent win in 2018.

Guaidó was recognized as the legitimate leader of Venezuela by more than 50 countries, including the United Kingdom, and he was the one who requested that the gold not be handed over to Maduro's government, arguing that it would be used for corrupt purposes. He probably had a point.

In the case of Argentina this risk is more related to creditors like Burford in the YPF case, like I mentioned in Pesos No More:

The downside of this measure is that Argentina still has to pay around $16+ billion for the YPF nationalization, and since this gold is located abroad, it could potentially be seized by Burford if judge Preska allows it.

However, the real threat that this poses to the gold reserves located abroad is minimal (for now), since Burford first needs to prove that YPF is an “alter ego” of President Javier Milei’s government:

Burford is currently seeking further information on whether YPF is an alter ego of the Argentine government. The company argues that Preska already dismissed claims against it and says Burford is trying to relitigate the issue.

If Burford is able to make that claim stick, then those gold reserves could be in embargo territory.

Autist note: Argentina has a history of embargoes, this is one of the most famous stories around the Paul Singer bond trade:

Final Thoughts

Of course the ROI of the whole ordeal has to be seen, and things like transportation, insurance, storage and so forth would have to be taken into account if it would simply be a matter of generating yield on the additional gold reserves, as minister Caputo stated.

Given the BCRA’s secrecy around gold trades, it is unlikely that we will get a full breakdown of the costs involved to move the gold bars offshore.

Because gold is considered a less risky asset than fiat currencies, it usually offers lower interest rates. This is why the Gold Lease Rate for the past years is not that great, so it is not very likely that this additional 10% move abroad was made from a yield perspective:

However, the gold reserves will be very useful for repo swaps that the BCRA can use for maturities in 2025, like Argentina has done so many times before in the past.

Like those times before, we will only learn about these trades after the fact. Until that moment, it will be interesting to see what speculative stories media outlets come up with in the meantime.

See you in the Jungle, anon!

Other ways to get in touch:

X/Twitter: definitely most active here, you can also find me on Instagram but I hardly use that account.

Nostr: increasing my posts here, my npub: npub1sngpxenyrddqvnusf02fls8yl0ja3s373md9lmfkej2l0h6saz6qvglthh

1x1 Consultations: book a 1x1 consultation for more information about obtaining residency, citizenship or investing in Argentina here.

Podcasts: You can find previous appearances on podcasts etc here.

WiFi Agency: My other (paid) blog on how to start a digital agency from A to Z.