The Bermuda Triangle of Money Flows

An overview of how to get money in and out of Argentina

Welcome Avatar! One of the most difficult feats in a country with a bricked (or now BRICS, lol) firewall of capital controls is moving money in and out. Unless you want to take a 50% hit due to different exchange rates or leave a DNA sample to prove the money is yours, the legacy banking system is not your friend. An overview of the Bermuda Triangle of private capital flows in Argentina.

One of the first questions people ask when they pike an interest in potentially investing in real estate in Argentina, is how to get the money there without being taken to the Argentina Central Bank cleaner first.

We will go from easy to hard in this overview.

Offshore wire

This option is by far the easiest, and it means that the money never even touches Argentina. It is perfectly legal and the ideal scenario.

In order for this to be an option, the seller of the house must have a US or EU bank account — many Argentines do have these, so depending on their situation this could be an option when buying real estate.

Sometimes bigger real estate agents will offer this service into an escrow account they own, and they will go through one of the options below in order to get the cash to the owner in case he or she doesn’t have a foreign bank account.

With an offshore wire you only pay the wire fees, and locally in Argentina you pay the taxes on the deed, notary fees and realtor commission etc (so you would still need to get about 8-10% of the value of the property into Argentina, depending on your costs).

Cash Benjamins - no fee

Carrying cash US tokens is by far the easiest way to get money in and out of the country.

The downside is that it is limited to $10k per person, so buying a house with that will be tough, unless you feel like doing 10-15+ trips or wouldn’t mind the risk of getting caught with more than $10k, like these bible smugglers today:

Wouldn’t recommend trying the smuggle route, it just isn’t worth potentially losing your Benjis over versus paying a 2-3% fee with another option.

Western Union

If you’re not planning to send more than $12k/year, you can use Western Union. WU gives you the blue rate or a rate close to the blue rate. Sometimes with big rate swings, it can take them some days to catch up and their rate lags behind.

The downside here is that WU will not give you cash USD, only pesos, so if you need that then you would still need to swap those pesos back to USD bills at a cueva (see next option), which basically makes it more expensive because you’d be paying the WU fee + Cueva fee.

Also not useful in terms of total amounts, since they are quite low if you want to get enough USD in to buy a house.

Still a good option if you need cash pesos in Argentina. Also if you have residency and a bank account, WU now offers to send the peso funds directly to your account, which saves a lot of time compared to standing in line at a WU agency.

Cueva (Cash/Wires/Crypto) - 2-4%

This is by far the most used option in Argentina. I won’t discuss the ins- and outs of the whole cueva world, if you want to learn more about the mechanics I recommend to read this article, which goes through them from start to finish:

The main breakdown is this:

Cuevas take pesos and dollars, and swap them at the parallel market rates. Some regular transactions for a 3-4% fee include:

Cash USD —> Pesos (and vice versa)

USDT —> Cash USD (and vice versa)

US Bank Wire —> Third party bank in US —> Cash USD or Pesos (and vice versa)

So in the case you need to get dollar bills here, options 2 & 3 will come in handy.

ADRs / Exchange through MEP or CCL - 4-6%

For this operation, two types of exchange rates are used: the CCL (Contado Con Liqui) dollar and the MEP (Mercado Electrónico de Pagos) dollar rate. The latter is also used as the exchange rate for foreign credit cards.

Both of these rates are legal, although they do not respond to the formal price of the dollar established by the Central Bank, which is the “official rate”.

Both the MEP and the CCL rate are the result of stock market operations that involve buying a bond (or shares in the case of the CCL) in pesos and selling that same paper in dollars. This can also be done to sell dollars and switch to pesos. These rates are often referred to as “financial dollar rates”.

The MEP dollar is always carried out within the Argentine market. In other words, the saver/investor buys a bond in pesos and sells it in dollars within the Argentine Stock Exchanges and Markets (ByMA). New restrictions are in place since a few months: a seller of these bonds cannot use these dollars within the next 15 days, to avoid consumers from using this as a currency arbitrage trade.

The CCL dollar, has an international component, which allows the saver to have their dollars in a foreign account. The saver buys a stock or bond on the local ByMA market and liquidates it outside the country, so his dollars will remain in an account located abroad. The opposite can also happen, that is, that the person has an asset abroad and liquidates it in Argentina in case he needs to bring money from abroad.

There are third party brokerages that take care of these operations for a fee. Even though the amounts can be significantly higher in this option, so is the fee (3-6%), probably due to the degree of sophistication of the operation and the need of official brokerage accounts in both jurisdictions.

The rates for these operations also depend on the supply and demand (in March they reached 6%, but since then rates have decreased)

The CCL dollar is usually somewhat more expensive than the MEP and sometimes even exceeds the blue rate, since the investor is willing to pay a premium to get away from Argentine risk.

The CCL can be used through bonds, shares, local treasuries or Argentine Certificates of Deposit (Cedears, which are basically the inverse of ADRs, US stocks listed on a local Argy exchange).

As an example, someone can buy a GD30 bond in pesos and sell it as GD30C in his account in the United States and vice versa. Banco Galicia and YPF shares or Cedears such as Apple and Amazon are also widely used for this type of transaction.

In the case of a CCL transaction, there is a waiting period (called parking) between the moment a share or stock is purchased in pesos and is settled abroad in dollars. In the case of selling dollars to convert to pesos, there is no parking period.

Sending an International Wire

Feeling adventurous and wouldn’t mind losing your money in a bureaucratic loophole? If so, this option is recommended.

Sending an international wire to a USD account in Argentina is the closest thing to financial suicide: the wire comes in at the BCRA, is then subject to all sort of checks, likely to undergo some form of Central Bank skimming to prop up lacking reserves, and before the receiving bank will release the funds you will have to send DNA samples and prove ancestry lineage going back 3 generations.

Of course this is a bit exaggerated, but it feels close to reality.

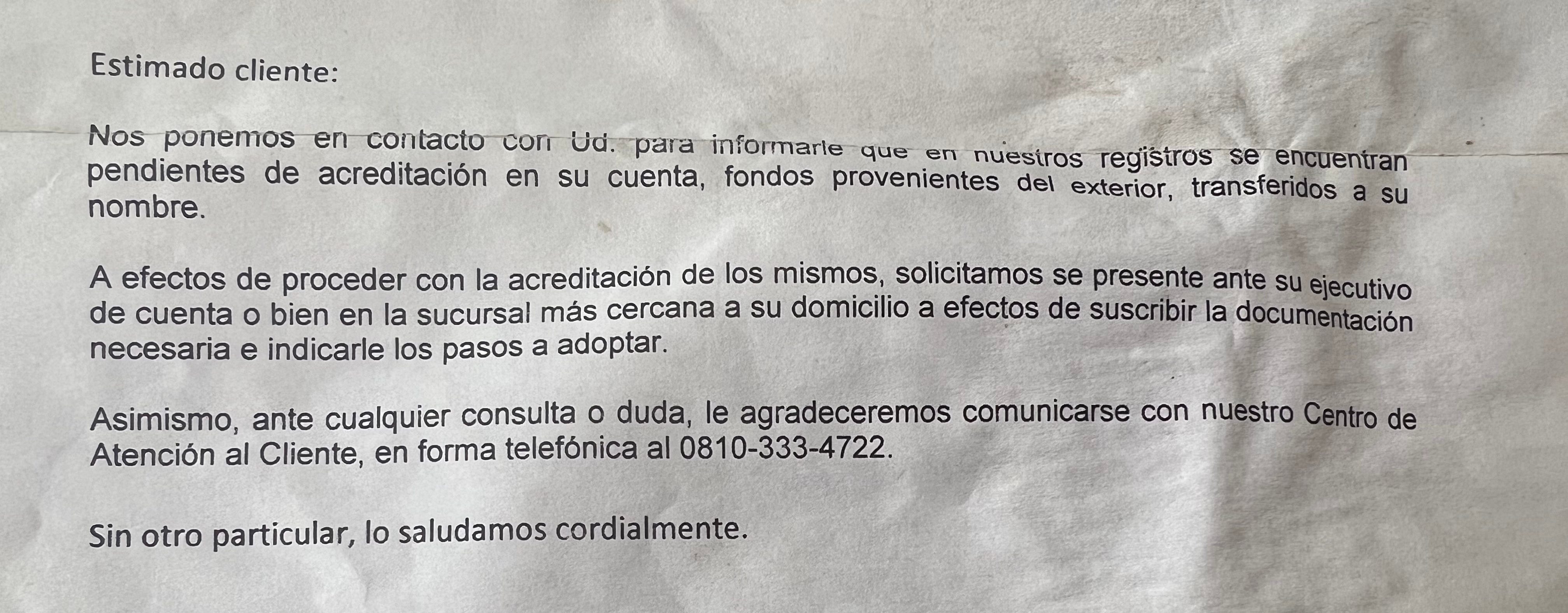

Just as a test to see what would happen, I once sent $120 USD from an offshore account to my local USD bank account in Argentina.

This was the sequence of events that followed after that wire transfer:

After a few weeks, I received a notification from the bank by post (yes, regular post dropped off at my doorstep). I was never notified in my online banking account or by email.

In the notification, the bank wanted me to contact an account executive at the bank:

After contacting the account executive, he sent me the following documentation steps that were necessary in order to release the funds into my account:

You can probably understand why I decided that the time needed to get all this documentation was more precious than those $120 and I left it at that, without the funds ever being accredited.

Still feels wrong to have donated that amount to HSBC, but at the same time I refuse to go through that administrative hellhole for that amount.

That about breaks it down in terms of inbound money options. Let me know if I missed one or if you have additional questions in the comments.

See you in the Jungle, anon!

Final note: If you haven’t read my series on real estate in Argentina yet and you’re interested in buying property, I recommend starting there first:

How are the banks now? I don't which one to choose for ease of transfers to and from the US. You mentioned you bank with Galacia (or because HSBC was bought out by Galacia).

For ease of use, which bank is the least horrible for expats here?

Great read. Maybe the laws are different but I've brought in over $80,000 at one time. I just declared it. I was buying a property and the seller wanted to sell really quickly so I brought it in. I had a certified and notarized letter from my bank stating it was withdrawn for the purpose of buying real estate. I didn't have any issues at all. I had a security guard meet me at the airport and it was uneventful.