Dollarization Scenarios for Argentina

Some scenarios for the peso and dollarization after the elections on Sunday

Welcome Avatar! As the general elections creep closer, now is a good time to go over all possible scenarios in terms of monetary outcomes for Argentina. Some outcomes are basically set in stone — like the implosion of the peso ponzi — whereas others, like dollarizing the economy, depend on a specific candidate winning the elections. Let’s dig in.

The Current State of the Greenback in Argentina

As mentioned previously in A Tale of Two Currencies, Argentina is de facto dollarized in many different areas of the economy:

The tale of two currencies for Argentina is the one between the dead presidents on the almighty dollar bills on the one hand, and the fauna and occasional dead president of the current peso notes on the other.

[…]

In Argentina, all items that can be used as a store of value, are priced in dollars. This goes for real estate, cars, and even their own currency, the poor old peso. The street rate of the peso against the dollar (dólar blue) is front page news every single day.

If you have every bought any bigger asset in Argentina, it is very likely that you’ve done so by paying for it with physical dollar bills.

In fact, Argentina is one of the most “dollarized” countries when it comes to physical dollar bills in circulation: an estimated 10% of all existing USD bills circulate in Argentina:

Estimates of 2020 stated that Argentine savers have around $200 billion USD in paper dollars, which means that the country owns 20% of the physical dollars that circulate outside the United States.

The dollar as a store of value to flee from the peso is so significant that in Argentina there are more physical dollars per capita than in the issuing country itself, the United States: 4400 USD per capita.

")

The 2nd highest per cap Latam country is Panama with 650 USD per capita, and while Panama is a country with a dollarized economy, Argentina isn’t (at least on paper).

More recent calculations estimate that Argentina is home to as much as 244 billion cash dollars. At the moment of writing 244 billion is easily 10 Argentina Central Banks if you take the current reserve levels into account, and it represents around 50% of Argentina’s annual GDP.

Whatever the exact number of circulating Benjies is amongst private citizens, safe to say there are enough to go around and create a circular economy.

Of course that is not the way a dollarization would work, and many of these dollars are concentrated into a few hands (mainly from the middle class up to the elites). The poorest in society would like to save in dollars, if only they had some pesos left at the end of the month.

Dollarization Scenarios

So how would a potential dollarization work? Unfortunately there is not a lot of clarity on how Milei’s team would dollarize the economy given the current circumstances.

The fact that the economy is so volatile in this election year makes it even harder to predict what kind of reserves will be handed over to the next government.

In terms of how to dollarize the economy, there are a couple of options:

Take on debt to convert the peso debt ponzi (Leliqs) into USD without defaulting (see an explanation here);

Apply a Bonex 2.0, defaulting on a big chunk of the peso debt and restructuring it (this would mean degens who gambled on the 300% peso APY would get rug pulled, see more about that in this article);

A combination of 1 & 2;

Convert all deposits in pesos to dollars, decreeing that all pesos are now dollars.

This “argendollars” scenario would be the least genuine, but some have mentioned this as a possibility in the face of a complete lack of dollar reserves, so that is why it’s included in the list.

However, one of the main economists on the Milei team already mentioned that if faced with that scenario of not having sufficient dollar reserves available, dollarization is off the table.

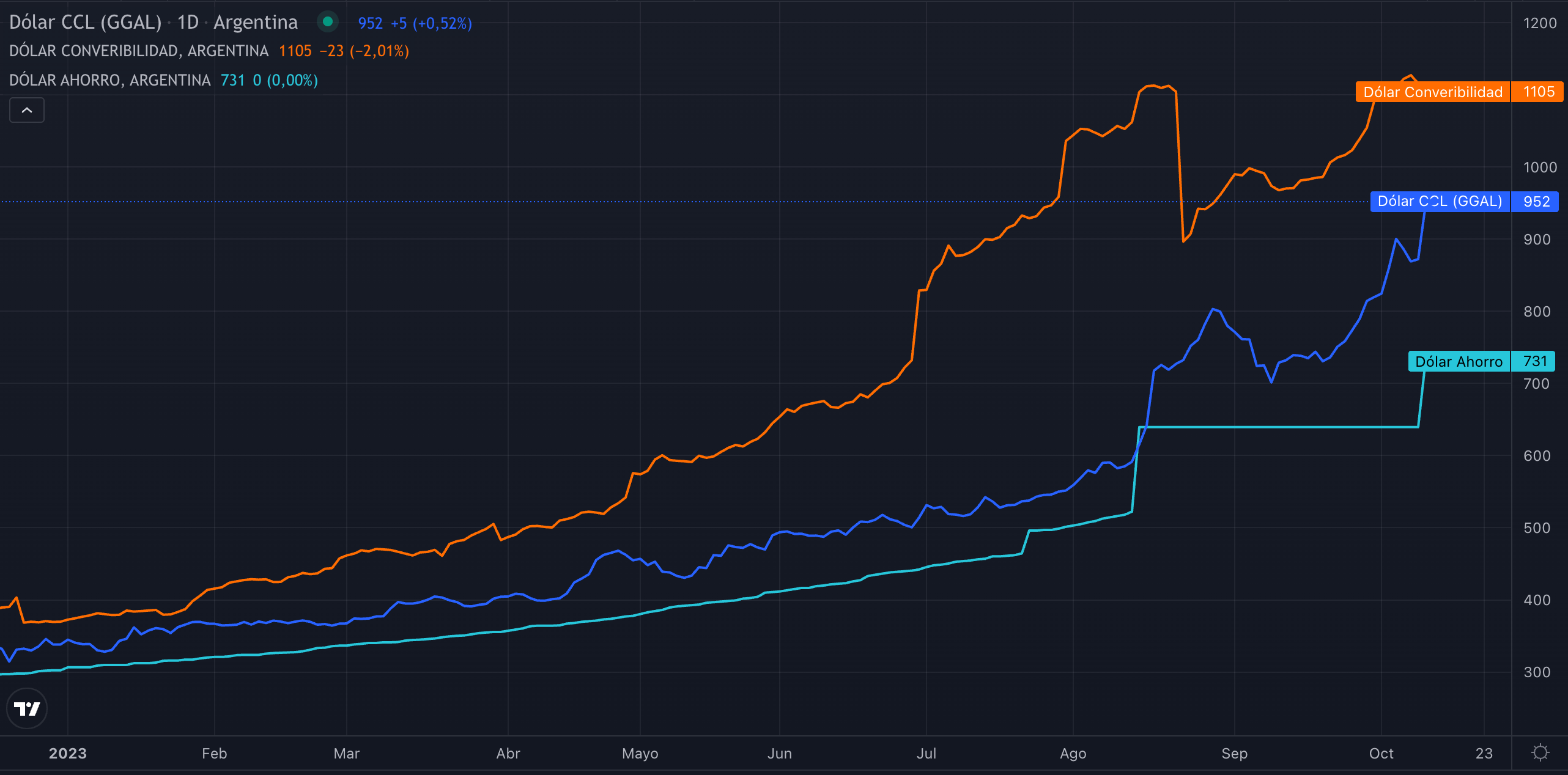

No one can say for sure what the exchange rate would be of a full dollarization, because so many elements have to be taken into account. Estimates range from the current blue dollar rate to a 2x or 5x from there.

As a frame of reference, the Convertible Dollar rate is currently at $1,100 pesos per dollar. This rate only takes into account the amount of pesos in circulation against the dollars in BCRA foreign reserves, nothing more. For a full dollarization many additional liabilities in pesos have to be taken into account.

Unconstitutional?

None of the scenarios above take into account the legal aspect of a dollarization.

According to most opponents, a full dollarization would be unconstitutional if it implies the removal of the local currency printed by the BCRA.

Horacio Rosatti, President of the Argentina Supreme Court, stated the following in September:

“If dollarization eliminates the peso it is unconstitutional.

What is the currency of a country? The currency that it prints: it can be the peso, patacón or whatever. If dollarization eliminates the Argentine currency it is unconstitutional.

If I abandon one currency and go entirely to the other, it is a path that, according to my interpretation, is unconstitutional.”

But, where there’s an obstacle in Argentina, there’s usually a way around it. This brings us to the “Argentino Oro”.

Argentino Oro

The “Argentino Oro” is an Argentine currency that was born 142 years ago in 1881, by order of the National Congress. This currency could potentially be the key ingredient for Milei’s team to carry out the dollarization if he is elected on Sunday.

Today this currency survives as an investment instrument, and is mainly used to calculate compensation for air and shipping accidents.

This relic was implemented prior to the creation of the Central Bank, and could be transformed into the legal twist that allows Argentina’s economy to be dollarized without going against the text of the National Constitution.

")

The Argentino Oro is Legal Tender according to Ley 1.130 currently in force. The BCRA publishes its price every trimester. Its issuance does not depend on Argentina’s Central Bank but on the Congress.

20 years ago during the 2001 crisis, while trying to rescue the 1:1 dollar peg, a proposal to dollarize the economy using the Argentino Oro was one of the alternatives on the table.

The problem, as they understood at that time, was that going from the convertible peso to a full dollarization could clash with the Constitution which, in article 75, obliges the National Congress to issue currency and “defend” it.

The proposal does not mean under any circumstances that it is proposed to use gold as money in Argentina. Placing the Argentino Oro in the role of national currency would not even imply minting a single new coin. Given the country's difficult financial situation, it would be almost as utopian to accumulate gold as to accumulate more dollars in reserves.

Using the Argentino Oro is just a legal twist: the base of existing coins that were minted almost a century and a half ago is enough. Argentina would then switch from the current peso to the Argentino Oro on paper as the national currency, without actually using it.

The Argentino Oro adoption would only comply with the Constitution and thus prevent a Supreme Court ruling from overturning dollarization. Hecha la ley, hecha la trampa.

Dollarization could continue its course with all the technical, financial and monetary problems it faced beforehand. But without constitutional obstacles.

Likelihood of Closing the BCRA

So what about using the chainsaw for the Central Bank?

The closing of Argentina’s Central Bank could probably only be completed by using the Argentino Oro trick, since the issuance of that gold friend does not depend on Argentina’s Central Bank but on Congress.

In Argentina’s Central Bank (BCRA) mandate (Article 3), it specifically says that:

“It is the primary and fundamental mission of the Central Bank of the Argentine Republic to preserve the value of the currency.”

The reaction to that phrase when locals read it or hear it, is usually unanimous:

This is why many locals think closing the BCRA would be a great step forward for Argentina, since it’s the main enabler for many of the country’s problems.

The BCRA is used as the limitless lender of last resort to fund public deficits, and it has burned many different national currencies to the ground throughout its history.

Fully closing it will still face a lot of opposition, so its role might be symbolic in a dollarization scenario, only publishing the Argentino Oro rates and the current state of foreign reserves.

Alternatives: Massa’s DevalueCoin

What are the alternatives? If you’ve been following Argentina’s economic history of the last century, you’re well familiar with those: slashing zeros, creating a new currency after $ARS inevitably implodes. After that, the show goes on, just with less liquidity and more debt.

During a debate this month, candidate Sergio Massa dropped that he has a plan for a digital peso, or DevalueCoin. During the debate, Massa explained:

"just as your children propose the possibility of trading with their cell phone or credit card on their online platforms, we are going to do it globally for all of Argentina.”

The minister added that this digital currency will be:

"accompanied by a laundering law that allows those who have money abroad to bring it and use it freely without new taxes."

Furthermore, according to Massa, the government would grant tax exemptions to those who use this digital currency.

With a good part of the national economic activity outside the formal circuit and dependent on physical cash, “a digital currency would generate tools to incorporate the informal economy into the formal circuit,” according to the Ministry of Economy.

Autist note: This is another step in the direction of a cashless society, something that is absolutely impracticable in Argentina at the moment, but forces in favor of this can’t be ignored. The IMF is also pushing for this, and in this article I wrote about this being one of the likely reasons why the BCRA is not printing higher denomination bills: to force people onto digital payment methods:

For now, according to Massa this “digital peso” would co-exist with the current forms of the peso.

")

In other words: this changes absolutely nothing, it would only provide a new vehicle for the peso with additional benefits if people want to enter a blanqueo (declare undeclared funds that the Argentine government doesn’t know about).

As of now, it is very unlikely that Argentines would trade their savings in Benjies for anything else, much less for digital pesos on a CBDC rails.

It is also questionable if Argentina could dollarize without additional external funding, or a peso debt (Leliq) default.

See you in the Jungle, anon!

It will be interesting to see how this plays out. Lots of ways to play it. I think another big Amnesty is in the cards to get locals with HUGE amounts of assets abroad. Almost all of my wealthy Porteño friends all are hiding tons of cash abroad in the USA and Europe accounts. Milei could do a sweep with the IRS to find all of these people and threaten them with harsh penalties if they don't bring it back.

I think just the threat of that would help bring in a TON!