Lionheart: Milei's First Year in Office

An overview of Milei's first year and upcoming challenges in 2025

Welcome Avatar! This overview of the first year of Milei’s presidency is a longer update based on the guest post published on BTB’s substack last week, including additional information for 2025 and a surplus measurement discussion. Let’s dig in.

Note: if you already read my guest post on BTB last week, the “Real or Artificial Surplus?” and the “Final Thoughts” sections at the end are new and updated in this article.

Even though some sceptics like Ian Boomer were certain that an “Argentina collapse was coming imminently” under Milei (tweet has since been deleted), and local bang haircut progressives assured “his government will not make it through Q1”, nothing could be further from the truth.

Now that Milei has been in office for almost a full year, let’s go over some of the key changes that are geared towards transforming Argentina from a bureaucratic inferno of protectionism into an economy that could be listed higher on different economic freedom indexes.

Rental Law

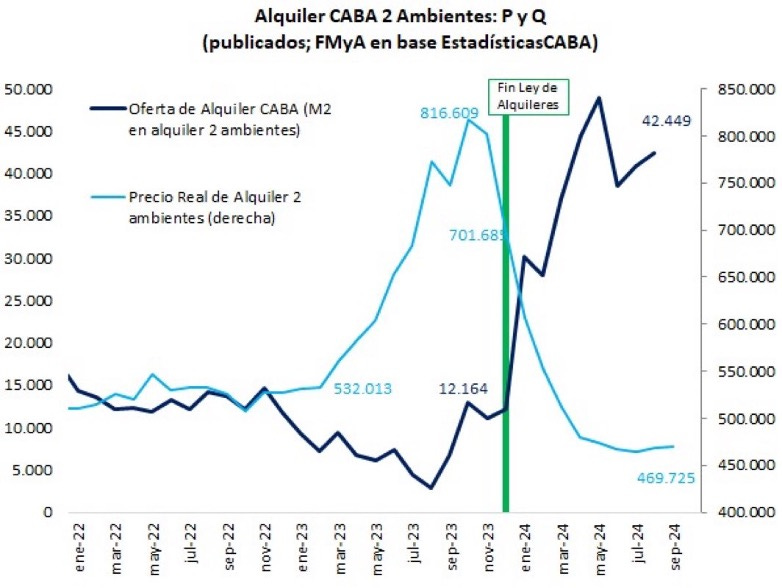

One of the first measures by the Milei admin was to issue an executive order to apply changes in the labor system, simplify some bureaucratic procedures to modernize the State and to repeal the Rental Law.

That last item alone has shown the power of the Milei deregulation better than any other measure: before, with the Rental Law in place, property owners were not allowed to increase rent prices more than once a year, and rents could only be charged in pesos.

Obviously, very few owners considered renting out their property under those conditions with a 300% YoY inflation rate, lol. Long term rental properties in pesos were very hard to come by, and owners rushed to furnish their apartments to convert them into STRs on Airbnb.

Repealing the Rental Law flipped this dynamic completely: now, rental contracts can be signed in any currency – including Bitcoin if you so wish – and the owner is free to determine when rents can be increased or not. The result?

The supply for long term rental properties at a fixed dollar rate increased by 189.77%, and a drop in rents across the board of -38.6%.

Since the market was flooded with Airbnbs, many owners decided that converting them back into a long term rental at a fixed USD rate would actually be more profitable. Funny how that works.

Ley Bases and Ministry of Deregulation

In June of this year, Argentina finally made its first step towards a more open economy and less State intervention: the Senate approved all chapters of the Omnibus Law package or Ley Bases with only slight modifications.

One of the most important items besides a 30+ year tax regime for investments of over $200M (RIGI) and further deregulation and state reform, was the fact that Milei was given emergency powers.

This is very common in Argentina, and usually these get extended throughout each presidency, which boils down to enabling the president to push virtually everything through by Executive Order. Normally presidents would receive 2 years of emergency powers at the start of their presidency, but since Milei doesn’t have a majority in Congress, the opposition pushed for it to be only one year. They are very scared to lose their privileges, and it shows.

The emergency powers were a godsend for the Milei administration, because now most deregulations can be pushed through by the Ministry of Deregulation directly without having to go through Congress first.

Yes, Milei created a Ministry of Deregulation, the original DOGE where Elon got the inspiration from.

Minister Sturzenegger is at the helm there, and he has a timer that counts the number of days Milei still has emergency powers so they can nuke as many government regulations in that timeframe as humanly possible.

This week, deregulator Sturzenegger launched a separate deregulation website, where citizens can notify the deregulation ministry of insane and backwards regulations that are ripe for destruction. Citizens can report the following:

Another big deregulation was at the tax collection office in Argentina: Milei dissolved the AFIP (IRS) and created a new, smaller collection agency. Directors' salaries by -90%, and salaries of lower-level authorities were reduced by -30%, while the total number of employees was reduced by -15%.

Elon and Vivek, take note.

Tax amnesty

One thing that is always in short supply (and in oversupply on the black market), is dollars.

Since such a large part of Argentina's economy runs in the shadows (estimates for the black market / below the table economy run from 40-55%), it's fairly common for each new government to try to get a hold of some of that undeclared money by offering a tax amnesty or blanqueo (literally: money laundering).

With more socialist-leaning governments like the previous admin under Alberto Fernández, few people to decide to declare any undeclared funds, and the tax collection on them is minimal since conditions tend to be less favorable.

The situation was completely different with a more fiscally responsible government: the Milei admin allowed Argentine mattress savers to launder up to $100k USD tax free, and everything above $100k would only be taxed at 5%.

With over US$ 20.6 billion entering the financial system through the tax amnesty, it was a real success, and for the first time private USD deposits were at a higher level than the international BCRA (Central Bank) reserves.

Many younger Argentines swapped their crypto to cash dollars – something fairly easy to do at black market money exchanges called cuevas – to later deposit those bills in a blanqueo bank account for laundry.

After the cutoff date, they were able to withdraw that USD in cash and buy crypto again. It’s funny to see cashiers at banks here do not even blink when you withdraw $100k USD in cash, that’s how normal dealing with cash is in Argentina.

The idea behind swapping the crypto for fiat instead of declaring the crypto itself is that this is a way to avoid the 15% capital gains tax in the future, plus all declared assets filed for the amnesty are valued at their valuation on December 31st, 2023, when Bitcoin was less than 50k. As you can see even when declaring undeclared assets, those savings will still be undeclared afterwards because they are in crypto again, lol.

The final numbers were 330,793 special laundromat bank accounts with a total of $20,631,000,000 dollars declared, so most people declared less than $100k to play it safe. An additional $30 million USD was declared in crypto assets.

In real ancap fashion, President Milei called for destroying the database of anyone who adhered to the tax amnesty, so it can’t be used against them in future administrations if they are short of cash and want to start auditing.

Surplus above all else

Milei's shock doctrine is mainly a fiscal shock doctrine. Curiously, and despite expectations, Milei has been gradualist in his monetary policy and very strict in his fiscal policy. Currency restrictions are still not lifted, but the fiscal surplus is non-negotiable.

The central point of the Argentine government's fiscal policy in its first 10 months has been zero tolerance for the deficit. So far, Milei’s admin has already accumulated 10 consecutive months of primary fiscal surplus.

Between January and October 2024, Argentina has already accumulated almost 1.7% of its primary fiscal surplus over GDP (in contrast to the deficit of 1.5% of GDP in 2023).

Once the interests of the gigantic debt inherited from previous governments have been paid, Argentina will achieve a surplus of 0.5% of GDP, which is well above what organizations such as the IMF recommend when handing out loans.

Just to give an idea of how unique this is in Argentina, here’s a graph of the fiscal deficit and surplus over the last 60 years:

Yes, that’s very little green, and the green from 2003 onwards was because Argentina had defaulted, which is not the case now.

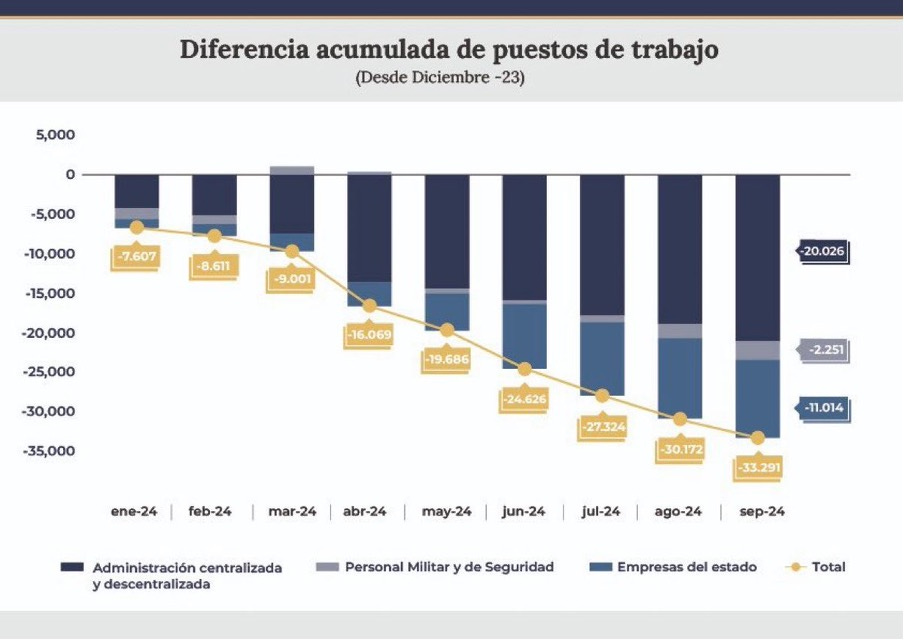

Most of this surplus was achieved by cutting government programs, ministries and secretaries, and by downsizing the total headcount of federal employees:

These kinds of measures, combined the monetary measures of pulling pesos out of the economy versus printing a new monetary base ever month, do not come without their short-term downsides: an overall slowdown in economic activity, and a short-lived recession in the first half of 2024.

From June onwards, industrial production started growing strongly and in September this was almost at the same level as in November 2023 (before the Milei government came into office).

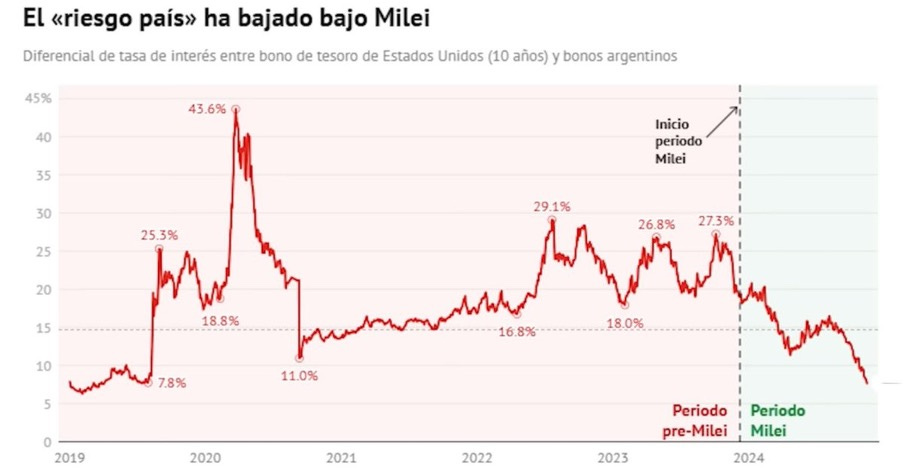

Country Risk

One crucial item to watch for most EM countries is the J.P. Morgan Country Risk Index, which measures the differential between the interest rate of a US bond and that of each country (specifically the 10-year bond). The higher the country risk, the higher the interest rates on dollar loans.

In the case of Argentina, country risk has plummeted after Milei started, due to the accumulation of fiscal surpluses and the relatively rapid emergence of economic growth – J.P. Morgan estimates that Argentina’s GDP will grow 8.5% in 2025, one of the highest growth rates in the world.

Inflation

After the risk of hyperinflation right before Milei started, his government decided to devalue the official peso rate, which was completely out of whack with the real-world dollar rate (official rate $360 vs $905 pesos at the blue rate, lol), which caused an initial spike in inflation in December (25.5% MoM).

After that, inflation has trended down thanks to winding down the peso debt ponzi at the BCRA and expectations are that inflation will hover around 30-50% for 2025. Still high, but a lot better than 300%.

Dollarization & Closing the BCRA?

Despite the potential outflow of dollars in the near term due to a tower of maturities in 2025, a few steps into the direction of either dollarizing or closing the BCRA have been completed thus far:

All BCRA debt was transferred to the Treasury;

No more peso issuance (still some, but compared to previous gvmts this is close to zero);

Local dollar-denominated bank accounts can now be used for everyday expenses in pesos;

The USD deposits of the private sector outweigh the BCRA dollar reserves for the first time in history

Different rates converging to ~$1,100 pesos per dollar

Closing the Central Bank will not be as straightforward as closing and restructuring the AFIP (IRS) office: in the Constitution there is mention of a Central Bank that has to issue currency in Argentina.

In Dollarization Scenarios for Argentina you can read more about how the Milei government might circumvent that, by focusing on the Peso Oro and delete pesos (ARS) from the central bank database altogether.

Milei’s idea is to stimulate currency competetion, and have citizens decide what currency they prefer to use. If the peso is deleted, that would de facto boil down to a dollarization.

Just to give an idea of how common it is in Argentina to transact or save in dollars, about 17.2 million Argentines have a dollar bank account. This is roughly half of the adult population. The dollar is not going anywhere in Argentina, and when you mention a BRICS currency most Argies shrug, buy USDT or cash USD bills at a cueva, and laugh. Stablecoins are a day to day thing at cuevas, although Millenials do increasingly save in Bitcoin.

Real Estate in Argentina

Since the peak of the RE market in 2018, m2 prices in Buenos Aires had dropped -50% in real terms in dollars until around October 2023. In hindsight, that was the bottom, and prices have since increased, in some neighborhoods increases are over 20-30% YoY. In October 2024, average prices on deed have DOUBLED compared to October 2023.

Pretty insane, but that’s the Argentina rollercoaster.

Around 10% of the tax amnesty deposits mentioned earlier have already been withdrawn from the bank, and a lot of those dollars will convert into real estate. This dynamic, combined with rising wages in real dollar terms and the start of mortgage credit under Milei (300% more mortgages YoY), is a perfect set up for this uptrend to continue.

If you’re interested in property info on Buenos Aires you can find several guides and updates here.

Other downsides?

Naturally, when coming out of 2+ decades of socialist protectionism, this doesn’t come without downsides. Argentina is definitely not sprayed over with libertarian rainbows all of a sudden. There is still a lot to improve, but the course is clear and steady.

Milei’s La Libertad Avanza party still has some growing pains in terms of internal power structures and political infrastructure, which is logical since it has only been spun up not even three years ago.

A recent falling out between Milei and vice president Villarruel is an example of some of the frictions at play, and shuffling of key positions has happened a few times already.

For the overall population of peso earners and digital brokemads alike, life has become a lot more expensive due to the peso appreciating thanks to the fiscal and monetary measures taken by Milei. Steak flexing on the gram is not what it used to be.

Even though inflation is down significantly, if a speeding car goes from 300mph to 60mph, it is still moving forward, and so are prices. And with a stable or even appreciating peso against the dollar, life just isn’t that much of a bargain anymore. That said, 2019-2023 was the anomaly in terms of ultra cheap prices for Argentina, and prices are now getting closer to the historic norm.

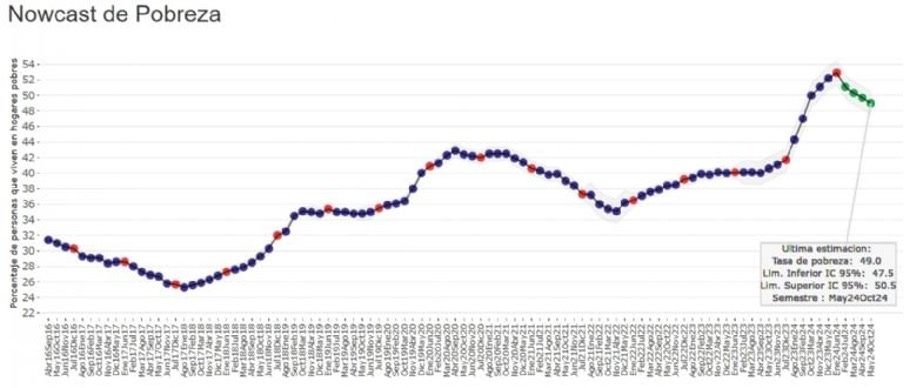

Ripping off the bandaid of the money printer initially cause the poverty rate to increase to over 50%, but this is now gradually declining and closer to 47.5%:

Local salaries are now finally increasing in real dollar terms and even outpacing inflation in the last 3 months, and the expectation is that this trend will continue.

Once deflation hits in, prices should decrease. The main thing to watch here is the speed at which these things happen, while still having a devaluation crawling peg and currency restrictions in place. You can read more about the dangers of this exchange rate dynamic under currency restrictions here, and in the past maintaining a crawling peg for too long with a relatively high peso has gone south more than once for Argentina. Key will be that the Milei team lifts the restrictions as soon as possible early 2025, with a floating exchange rate.

Argentina now has all the elements in place to move to a free-floating exchange rate in the next 12 months: 1) a trade surplus, 2) a fiscal and financial surplus, and 3) the economy is starting to grow and will grow at its highest rate in 15 years in 2025.

This will also boost foreign investments, which, besides mining and oil & gas, are still relatively low. Many international companies are “waiting it out” to see what the outcome of the October 2025 midterm elections will be before making a move.

So far, many different consultants estimate that Milei’s LLA and the PRO will get to more than 50% of the votes, which would be a landslide. Still 37% of Kirchernism/Peronism, but hey, you can’t change that overnight, and history shows that a hardcore 30% will never switch sides no matter how successful Milei is.

Real or Artificial Surplus?

After last week’s This Time is Different article, which was a title chosen on purpose because it remains to be seen if this time is different, and that is one of the most dangerous words in finance, reader Quipus Capital pointed out the following in the comments:

“Respectfully disagree. There is no surplus, because the financial deficit does not account for capitalized interest. If a US GAAP or IFRS company does not record capitalized interest on the income statement that is called fraud. If you account for capitalized interest, total deficit is closer to 10% of GDP.

You do not mention the massive instability of the peso when the Central Bank has negative reserves while the aggregate monetary base has grown 100%+ YTD. It only takes a dollar sneeze to generate a Minsky moment, and the closer you get to the midterms the riskier this will get.

For an investor doing carry the question is super simple: do I keep two months more of carry to make 5%, or dollarize now at the lowest FX on record?”

Sometimes enthusiasm for new policies and economic management can blur some of the hidden traps that would precisely unwind the peso carry trade like it has in the past: an artificially overvalued peso making Argentina expensive but providing purchasing power to Argentines when they travel abroad.

The main narrative against this happening from the official government stance is that there’s a surplus, so let’s dissect the comment above to see how that surplus could be interpreted differently and if it could potentially become a deficit.

Autist note: you can find a more in-depth overview of both the carry trade and the focus of Milei’s administration on a fiscal surplus here:

At the start of Milei’s term, the BCRA (Central Bank) debt, the famous Leliq peso ponzi, was printing a new monetary base every 1.5 months. First, interest rates were lowered considerably, and afterwards these debt instruments were transferred to the Treasury under different names and rates.

A part of that Treasury debt is now called LECAPs. Those Lecaps capitalize interest daily, and are structured as bullet repayments: a one-time lump-sum repayment of the outstanding loan plus interest.

Currently when calculating the surplus, the government’s numbers do not take the interest on those bullet bonds into consideration until repayment. According to some economists, Argentina’s interest levels with these bonds taken into account would be at three times the reported surplus, which would mean the deficit is twice the reported surplus.

Are you for real Mara? The reality is somewhere more in the middle.

This calculation by consulting firm 1816 includes ALL debt + accumulated interest, such as the Lecap, Boncap, Lefi instruments:

So even by the most conservative of measurements, Milei’s surplus is still there.

The 1816 report seeks to approximate the “genuine” fiscal surplus, and states that between January and October 2024, the national State had an accumulated primary surplus of ARS$10.3 trillion, paid interest for ARS$7.4 trillion and, therefore, had a financial surplus of ARS$3 trillion.

In that same period, the capitalization of Lecap, Boncap and LeFi was around ARS$10.4 trillion, which makes some analysts suggest that the Government actually had a financial deficit.

However, of the ARS$10.4 trillion in interest capitalized on fixed-rate bonds during the year, more than 90% — exactly ARS$9.6 trillion — can be explained simply by the interest rate that compensates for inflation. This last part is crucial, and goes back to the initial comment above: inflation for 2024 will still be hovering around 120%.

The capitalization explained by a positive real interest rate was ARS$0.8 trillion, calculated by using the methodology used in public accounting for the capitalization of interest.

1816 concludes that the financial result of the treasury was still positive by around ARS$2.2 trillion.

When looking at the monetary base until October 30, we see a similar stable picture of no significant increase:

This does not mean that the rest of Milei’s administration will be smooth sailing, and inflation will not return. There are still many variables that can cause this to happen. Last week, the BCRA lowered interest rates and the expectation is that this will also happen with future Lecaps and other peso debt issuance.

Key for the Milei administration will be to increase net BCRA reserves, which are still negative.

In 2025, there will be no more blanqueo (tax amnesty), which accounted for 0.1% of GDP collected this year. Other revenue streams like the Special Regime for Personal Property (0.2% of GDP) and the debt moratorium (0.2% of GDP) will also be absent. Furthermore, the PAIS tax (1.1% of GDP) was also eliminated.

Final Thoughts

Going cold turkey, the Argentine economy has suffered considerably in the first two quarters of 2024 after the withdrawal of stimuli in the form of unbridled public spending carried out by the government of Javier Milei.

But removing the hyperinflationary helicopter money and the State from the economy has helped to achieve a fiscal surplus that was unimaginable a year ago. It helped to control inflation that was already bordering on hyperinflation and, although it has generated a recession, it looks like that recession has barely lasted two quarters.

As noted above, there are multiple ways to skin the surplus results, and when taking all debt instruments like the Lecaps into account + accumulated interest, Milei is actually still running a surplus.

However, the negative net BCRA reserves could come and bite the carry traders in their hinds if they keep in the peso trade for too long, potentially blowing up the exchange rate again once the cepo restrictions are lifted — unless the current dynamics change. There is a reason why Caputo and Milei are so hesitant on lifting currency controls: history has shown that in Argentina a potential flight to the dollar is always present.

Since the start of his presidency, many analysts have predicted Milei’s future demise multiple times given the negative short term outlook — this ranged from Argentina defaulting due to debt levels, Milei’s party not getting enough consensus to govern and having to leave early, to not being able to lower inflation and so on.

But so far president Lionheart has show to have enough control, with good decisions combined with some luck — in Argentine Spanish the expression is directly related to hinds: tener culo — so if anyone could pull it off without significant exchange distortions or a Minsky moment, it would be Milei.

One thing to always keep in mind was the state Argentina was in right before Milei came to power. The gap in the black market and official exchange rate was over 200%, inflation was running towards 300% YoY and hyperinflation was imminent with the degens at the BCRA printing an additional monetary base every 1.5 months due to local debt instruments in pesos.

In the words of minister Guillermo Franco:

"We are approaching our first year in office; a year marked by firm decisions, profound transformations […] which steered Argentina towards a future of growth, development and freedom. In these 12 months we have avoided an unprecedented crisis and, little by little, we are beginning to see concrete results that are reflected in macroeconomic solidity, the sharp drop in inflation, the reorganization of public accounts and the recovery of economic activity and wages."

The most amazing thing is that Milei was able to do all this virtually without any support in Congress.

Just imagine what is in store after the Midterms in 2025, which his party La Libertad Avanza, in combination with a PRO alliance, is set to win with over 50% of the votes. If that happens next October, you can bet on an even bigger chainsaw mowing through backwards regulations and a morbidly obese public sector.

The key will be if provincial governors play ball: so far, they have not cut any significant deficits, and most municipalities and provinces raised local taxes to make up for the loss in handouts coming from the national government.

Another thing to watch in 2025 is when currency restrictions (cepo) will be lifted, and what happens to the exchange rate afterwards. Argentina is very much a bi-monetary and practically dollarized country, so a lot depends on the local demand for crispy Benjamins.

Until then, we can expect to see a lot more ¡AFUERA!

See you in the Jungle, anon!

Other ways to get in touch:

1x1 Consultations: book a 1x1 consultation for more information about obtaining residency, citizenship or investing in Argentina here.

X/Twitter: definitely most active here, you can also find me on Instagram but I hardly use that account.

Podcasts: You can find previous appearances on podcasts etc here.

WiFi Agency: My other (paid) blog on how to start a digital agency from A to Z.

Finally, I found someone who talks about what is happening in Milei Argentina in English. Much appreciated.

What I would also love to see is how this affects regular folks. If you toss lots of people out of the cushy govt jobs, if the poverty rate skyrockets, how do these people get by? Don't the welfare rolls skyrocket too?

Great write up as usual. Spot on target. Still not out of the woods but what has been accomplished so far is remarkable. If they are successful in the mid-term elections going to be unstoppable.